When Fear Peaks: The Psychology of Crashes, the Hyperscaler Oligopoly, and the Momentum-Quality Gap That History Always Closes

Fernando Sánchez's live analysis of the tech crash goes deeper than price levels. He explains the neuroscience behind panic selling, why hyperscalers are exactly as cheap as they look, and why the gap between semiconductor momentum and hyperscaler quality is historically unsustainable.

Markets are falling. Headlines are alarming. The amygdala is firing. This is precisely the moment Fernando Sánchez chose to go live — not to calm nerves with vague reassurances, but to explain, with neurological and fundamental precision, why experienced investors behave differently from everyone else when prices collapse.

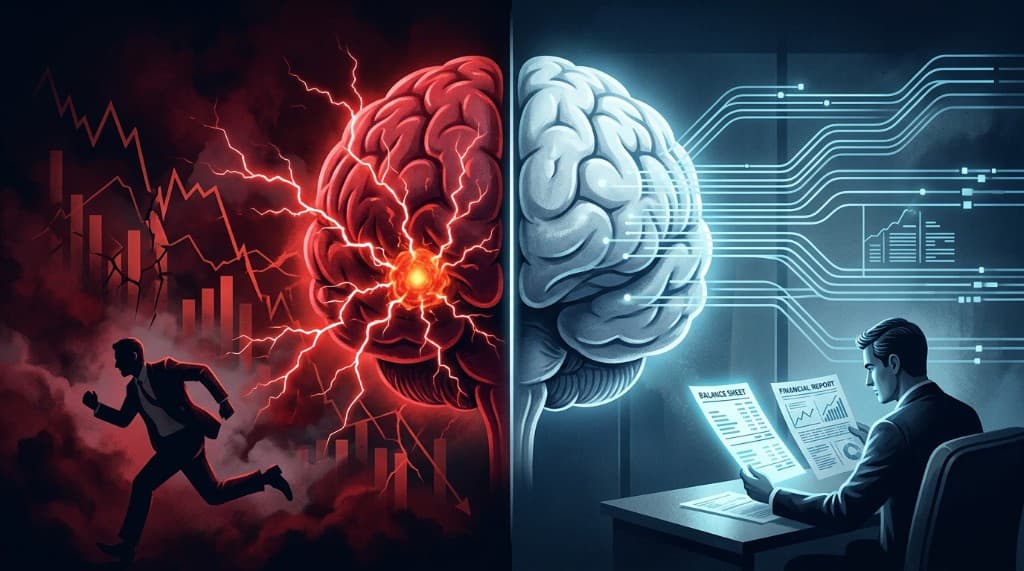

The Neuroscience of Bad Investment Decisions

Kahneman's two-system framework is not new, but it becomes urgently relevant on days when markets fall 10% before lunch.

System 1 is fast, automatic, and emotional. It evolved over hundreds of thousands of years to keep us alive in environments where hesitation meant death. A sudden loud noise, a charging predator, a falling KOSPI — System 1 treats them all as equivalent threats and triggers the same response: flee.

The amygdala — the brain's alarm center — floods the bloodstream with cortisol when it perceives danger. Markets moving violently count as perceived danger. The cortisol creates urgency, narrows focus, and pushes toward action: sell, get out, reduce exposure. This mechanism kept our ancestors alive. In financial markets, it destroys portfolios.

System 2 is slow, deliberate, and rational. It is also expensive in metabolic terms — the brain resists activating it unless compelled. On a day when everything is red and CNBC is running crisis chyrons, the path of least resistance for every neural circuit is to let System 1 drive.

The only reliable way to suppress the amygdala's interference is through knowledge. Specifically: knowing what a company is actually worth. If you know that a business with 46% operating margins and 17% annual growth is trading at 25 times earnings — historically inexpensive for those characteristics — then a 10% price drop does not feel like danger. It feels like a sale.

The investor who has done the fundamental work experiences the same volatility as everyone else. The difference is what the volatility means to them.

Three Factors Creating Today's Uncertainty

Markets, as Fernando points out, process uncertainty extremely poorly. They can handle bad news. They cannot handle not knowing whether news is bad or good or how bad or how long. Right now, three sources of genuine uncertainty are converging.

Geopolitical tensions in the Middle East continue to generate noise in energy markets. The Iran peace process, still incomplete, keeps oil price volatility elevated and provides financial media with daily alarm material.

Kevin Warsh at the Federal Reserve has explicitly abandoned forward guidance. The elimination of the dot plot — the roadmap that markets used to price future monetary policy — leaves traders without their anchor. Warsh has signaled the possibility of further rate hikes, potentially up to three, depending on incoming inflation data. Markets hate uncertainty more than they hate bad news, and "we'll decide when we see the data" is, from a market-pricing perspective, maximally uncertain.

Summer seasonality amplifies everything. Since mid-June, trading volumes drop as institutional desks go on vacation. Thinner markets mean that the same information moves prices further. What would be a 2% move in October becomes a 5% move in July. The Korea selloff — already a dramatic story on its own terms — was amplified by the technical reality that there were fewer buyers to absorb the selling.

The Korea story itself is worth a brief clarification. The KOSPI's collapse was triggered partly by extreme retail speculation in leveraged semiconductor ETFs and partly by a proposal to tax unrealized capital gains. Neither of these factors affects the fundamental outlook for US technology companies. But in a thin, anxious market, the contagion spreads on emotion, not logic.

The Hyperscaler Case: Buying the Pizzeria, Not the Oven

Fernando's central investment thesis comes down to an analogy. In the AI infrastructure build-out, there are companies that manufacture the ovens — the hardware, the chips, the memory — and there are companies that own the pizzerias: the platforms and cloud services that will eventually generate recurring, high-margin revenue from millions or billions of users.

The oven sellers have been the market darlings. Semiconductors attracted record capital inflows. Everyone chased the momentum. The pizzeria owners — Microsoft, Amazon, Alphabet, Meta — are intensively deploying capital, generating lower free cash flow in the near term, and being punished by a market that has a short time horizon.

Fernando's argument: this is precisely the moment to buy the pizzeria owners, because they are in the process of constructing an infrastructure oligopoly that will not be competed away.

Microsoft is the clearest case. Revenue growing at 17% annually. Operating margins at 46% — extraordinary for a company of this scale. And it is trading at approximately 25 times earnings, which by historical standards for a business with these characteristics is inexpensive. Azure's cloud backlog extends years into the future. Copilot is an entirely new revenue stream just beginning to monetize. The company is not speculative — it is a mature, high-quality compounder trading at a reasonable price.

Amazon is at its lowest EV/EBITDA multiple in recent years. The market is focused on the capital expenditure required to scale AWS, and the near-term compression of free cash flow. Fernando sees this through the correct historical lens: Amazon has done this before. When it invested in its original e-commerce logistics, the cash burn looked terrifying and the multiple collapsed. Then AWS emerged and the economics transformed. Supply Chain Services — the opening of Amazon's entire logistics network to third parties — is doing the same thing again. The margins will follow the investment with a lag.

Meta is the most extreme case. Trading at 17.4 times earnings — multiples that were last seen during the COVID crash. Its core advertising business generates operating margins approaching 50%. The metaverse investment has been the narrative that kept institutional investors away. But the business underneath is generating enormous cash and growing. July earnings are the next significant catalyst: the numbers will remind the market what it has been ignoring.

The Semiconductor Trap: Chasing the Carrot

The warning on the other side of the ledger is equally important.

Memory chip companies — the Microns, the SK Hynixes — are experiencing what looks like a golden moment. HBM demand from AI training is extraordinary. Orders are robust. Revenue is growing at rates that look spectacular.

But these are cyclical businesses. The demand they are experiencing today is not structural in the way that cloud computing demand is structural. It is tied to a specific phase of AI infrastructure buildout — the initial rush to construct training clusters. When that phase normalizes, and it will, the dynamics reverse rapidly. Cyclical businesses do not gently plateau; they fall hard and fast when the cycle turns. PER ratios that looked cheap at the top of the cycle turn out to have been expensive, because the earnings they were measuring were peak earnings, not normalized earnings.

This is not a prediction that the cycle turns tomorrow. It is an observation that investors currently in these stocks because of momentum — because the chart has gone up — are not protected by the same margin of safety as investors in high-quality compounders at below-average multiples.

NVIDIA sits in a special category. It is the clear market leader in AI training GPUs and commands a genuine competitive moat through its software ecosystem. But even here, the market is beginning to price in questions about the sustainability of hyperscaler demand at current volumes and the pace at which the next architectural generation can maintain the current extraordinary growth trajectory. At its current valuation, there is less room for disappointment than there was when the AI trade was less crowded.

The Gap That History Closes

The most actionable structural observation Fernando makes is about the divergence between momentum stocks and quality stocks.

Over the past 18 months, a significant gap has opened between high-momentum companies — primarily semiconductors — and high-quality companies with real, stable earnings — primarily hyperscalers. Momentum has vastly outperformed quality. This is not unusual; it happens regularly in bull markets. What is also historically consistent is that this gap closes, and it closes faster and more violently than most investors expect.

The closing mechanism is straightforward. Momentum strategies attract leveraged money. Leveraged money is forced to sell when volatility rises. When momentum stocks correct, the forced selling amplifies the move. Meanwhile, quality stocks — whose business fundamentals haven't changed — look increasingly attractive relative to their prices. Institutional money that was chasing semiconductors begins rotating toward the undervalued quality names.

We may be watching the early stages of that rotation right now.

The Strategic Conclusion

Fernando's conclusion is deliberate and clear: the investor's mission is not to find the next ten-bagger or to follow what is fashionable. It is to become a part-owner of excellent businesses at reasonable prices, and then to wait.

Short-term price movements are, on any given day, primarily information about the market's emotional state. They tell you almost nothing about what a business is actually worth or what it will earn over the next five years.

What tells you something real: revenue growth rates, operating margins, return on invested capital, the durability of competitive advantages, and the quality of management's capital allocation decisions. When these fundamentals are strong and the price falls because Korean retail investors were over-leveraged in semiconductor ETFs — that is not a crisis. That is an opportunity to buy better businesses at lower prices than last week.

The biological difficulty is real. The amygdala does not understand EV/EBITDA multiples. But the investor who has done the work — who knows what they own and why they own it — can watch the red screens without urgency, and sometimes even with anticipation.

Analysis based on Fernando Sánchez's live market commentary of June 23, 2026, on his channel Invertir desde Cero. This post is for informational and educational purposes only and does not constitute investment advice.

Explore the data

Check the latest congressional trades and active investment signals.