Meta Compute, the Toll Road, and Why Ackman Put 44% on Three Names

Two developments this week reframe the AI investment landscape. Fernando Sánchez analyzes Meta Compute — Meta's plan to sell or rent excess GPU capacity to third parties, turning already-spent capex into near-pure profit, with Morgan Stanley projecting $3-12 additional EPS by 2028 and stock targets of $872-$1,300+. Separately, Bill Ackman has concentrated 44% of his public portfolio in Meta, Microsoft, and Amazon — the 'toll road' owners of the AI era — while liquidating almost all of his Google position on valuation grounds. The hardware speculators are looking in the wrong direction.

The dominant narrative in AI investing in 2026 has been about hardware: which chip company wins, which memory supplier has the best HBM margins, which semiconductor ETF to own. Fernando Sánchez and Bill Ackman — working from different frameworks but arriving at the same conclusion — are both pointing at what they believe is the actual opportunity: the companies that will collect revenue on everything the hardware produces.

Meta Compute: The Capex That Pays for Itself Twice

Meta Platforms has been building at a pace that made many investors nervous. Hundreds of thousands of GPUs, data center capacity measured not in chips but in gigawatts, and a capital expenditure trajectory that showed no signs of decelerating. The standard criticism was that this spending was going into a black hole — that Meta was repeating the metaverse mistake, burning capital on infrastructure whose return was uncertain.

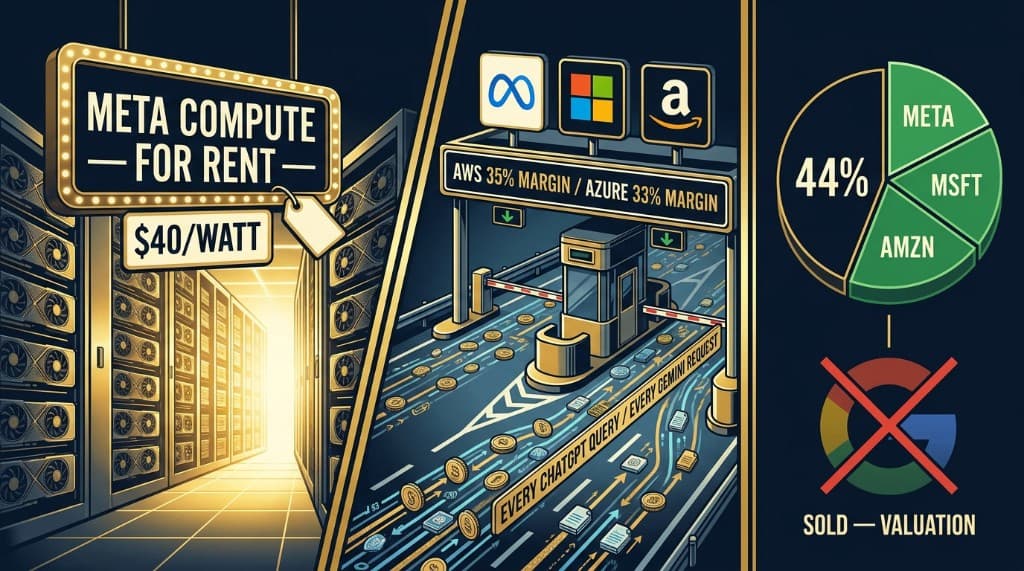

Meta Compute is the answer to that criticism. The plan is straightforward: sell or rent the excess compute capacity of Meta's data centers to third parties. Two mechanisms: an API service that sells access to AI models hosted on Meta's own infrastructure, and direct rental of raw compute capacity to businesses that want to run their own workloads.

The analogy Fernando Sánchez uses is a hotel. Meta has been building an enormous hotel — hundreds of thousands of GPU rooms — to serve its own guests: the advertising algorithms, recommendation systems, and internal AI models that run Instagram, Facebook, WhatsApp, and Threads. When internal demand does not fill every room, those empty rooms previously represented wasted investment. Meta Compute converts them into revenue.

The financial logic is unusually clean. The capex has already been spent. The data centers are built, the power contracts are signed, the cooling systems are installed. Every dollar of revenue from external compute rental flows almost directly to EBIT and EBITDA because the marginal cost of serving an additional external customer on already-built infrastructure is minimal. This is high-margin revenue that requires no additional capital outlay.

The scale of the infrastructure in question clarifies why the numbers can be significant. Meta's capacity stood at approximately 7.5 gigawatts at the end of 2025. It is projected to reach 12 gigawatts by the end of 2026 and 21 gigawatts by 2028 — three times the nuclear power capacity of Spain, running continuously to power AI computation. For reference, Alphabet has already signed agreements to rent compute capacity at an estimated $50 per watt.

Morgan Stanley has put specific numbers on what this means for Meta's earnings. At $40 per watt — a conservative estimate relative to current market rates — selling or renting just 1% of Meta's projected 2028 capacity (250 megawatts) would add approximately $3 to earnings per share. At 5% (1 gigawatt), the contribution rises to $11.8 additional EPS. Depending on the multiple the market applies to this new business line, these scenarios imply stock values ranging from $872 to more than $1,300 per share by 2028. Wells Fargo is more aggressive in its timing, suggesting that Meta could be selling 1 gigawatt of capacity as early as 2027, contributing $5.5 to that year's EPS.

The strategic implication is as important as the financial one. This converts Meta formally into a hyperscaler — a company that generates revenue by selling cloud computing services to third parties, not merely consuming its own infrastructure internally. It also eliminates the market's primary anxiety about Meta's capex. The investment now has a clear downside scenario: if Meta's own applications do not consume the capacity, the capacity gets sold at a profit. There is no longer a scenario in which the investment is simply lost.

Mark Zuckerberg's specific vision — demonstrated through Meta Compute — is that AI infrastructure is not a cost center but a revenue-generating asset that can serve both internal and external customers simultaneously. The market, Fernando argues, has not yet fully priced in this optionality. Margins above 40% become structurally achievable once compute rental is a meaningful revenue line alongside advertising.

Ackman's Toll Road: 44% in Three Names

Bill Ackman's Q1 2026 portfolio moves tell the same story from a different analytical tradition. Pershing Square's founder is known for highly concentrated positions built on deep fundamental conviction. His current positioning reflects a specific thesis about who wins the AI era.

At the close of Q1 2026, Meta, Microsoft, and Amazon together represented 44% of Ackman's entire public portfolio. This is not diversified exposure to the technology sector. It is a concentrated bet on three companies he believes the market is systematically mispricing.

The conceptual framework Ackman applies begins with a historical analogy. In 2000, Berkshire Hathaway was dismissed as "old economy" — it fell 50% while dot-com companies with no earnings and no revenues were rising 200%. The crowd was chasing the narrative, not the fundamentals. Ackman argues that a structurally similar dynamic is playing out today: investors are rushing toward hardware and semiconductor names while the companies that will actually monetize the AI infrastructure — Meta, Microsoft, Amazon — are being treated as yesterday's businesses.

The difference between 2000 and today is crucial, and Ackman makes it explicitly. The top 10 companies in the S&P 500 in 2000 represented approximately 37% of the index by market cap but generated a negligible fraction of actual earnings. The same companies today represent approximately 37% of the index — and generate 36% of actual S&P 500 earnings. These are not speculative promises. They are operating businesses generating enormous quantities of real cash, at margins that smaller competitors cannot replicate.

The "toll road" metaphor captures what Ackman sees as the structural advantage of the hyperscalers. Every time an application uses AI — every ChatGPT query, every Gemini request, every Claude interaction — computational tokens are processed on servers owned by Amazon (AWS) or Microsoft (Azure). Each token generates a payment. AWS cloud operates at approximately 35% operating margins. Google Cloud operates at approximately 33%. These are the tolls collected at every on-ramp of the AI highway, from every driver, every day.

Meta uses AI primarily internally — the advertising targeting algorithms on Instagram and Facebook that make each ad dollar generate more measurable return than any competitor can offer. This creates a flywheel: advertisers get better ROI, so they increase budgets, so Meta can charge more per impression, so advertisers get even better ROI. When Meta announced larger capex budgets and the stock fell 20%, Ackman doubled his position, describing the valuation as deeply discounted. He now holds a significant Meta stake at prices well below current levels.

Microsoft has become more than 15% of Ackman's portfolio after he added substantially in Q1. Azure's AI adoption is accelerating across enterprise customers at a pace that MSFT management has repeatedly described as exceeding internal forecasts. The RPO (Remaining Performance Obligations — contracted future revenue) stands at $627 billion, growing 99% year over year. This is not projected revenue. It is contracted, paid-for future delivery.

Amazon received a nearly 20% position increase. The logic follows the same infrastructure reasoning, compounded by the Supply Chain Services initiative — Amazon's decision to open its entire logistics network to third-party shippers, converting internal infrastructure into a revenue-generating service. The pattern is identical to AWS: internal investment, perfected internally, then opened to external customers at high margins.

The Google Decision

Ackman's Q1 moves include one decision that is particularly instructive for investors currently considering Alphabet: he liquidated almost his entire Google position, citing valuation.

This is not a bearish call on Google's business. Ackman's thesis about hyperscalers and AI monetization applies to Alphabet as clearly as it applies to Microsoft and Amazon. Google Cloud's 63% revenue growth in Q1 2026, at 32.9% margins, is exactly the toll road dynamic he is describing. Gemini, AI search, Waymo — the fundamental picture is strong.

The decision was strictly about price. At current levels, Ackman concluded that Google's valuation already reflects a significant portion of the AI upside, leaving insufficient margin of safety for the risk of being wrong on timing or execution.

This provides useful calibration for investors considering an Alphabet position. The business is excellent. The AI thesis is intact. The question is price — and at $345-352, one of the most disciplined fundamental investors in the world has decided the margin of safety is insufficient. The correction that brings Alphabet toward its Fibonacci retracement zones — $276 to $301 — would represent exactly the kind of valuation compression that converts a business Ackman admires into a position he would hold.

The hardware cycle will peak and rotate. The toll road does not stop collecting when the hardware cycle turns. That is the investment case for the three names Ackman has committed 44% of his capital to — and the same case that justifies patient positioning in those names, at the right price, for investors willing to wait.

Analysis based on Fernando Sánchez's channel content from July 2026. This post is for informational and educational purposes only and does not constitute investment advice.

Explore the data

Check the latest congressional trades and active investment signals.