The Memory Crash, the KOSPI Sweep, and Why S&P 500 Is Heading to 8,000

Fernando Sánchez documents the memory sector's two-week collapse: SK Hynix -26%, Western Digital -32%, Micron -25%, Seagate -29% from recent highs. José Luis Cava explains why it is not done yet, applying Dante Panzeri's football concept of 'the dynamics of the unexpected' to the KOSPI: the index must sweep every investor who entered since May — exhausting them psychologically — before a genuine bottom forms. Meanwhile, the S&P 500 case for 8,000 rests on a simple calculation: 6.2% nominal growth against a 4.5% bond yield implies 170 basis points of monetary stimulus that must find its way into equities.

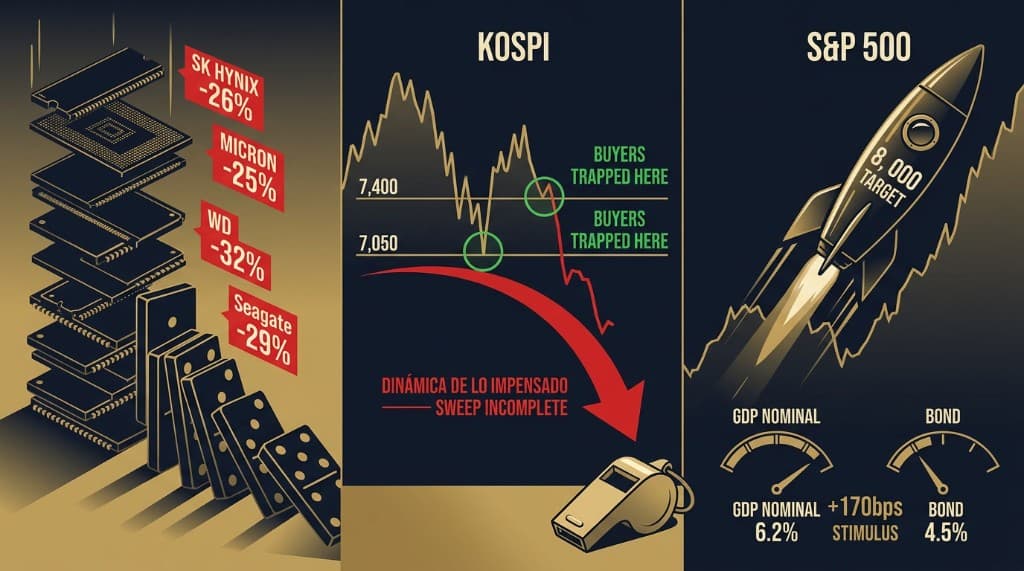

Two weeks. That is how long it has taken the memory semiconductor sector to give back a significant portion of the gains it built over months. The numbers from Fernando Sánchez's channel this week document the damage precisely: SK Hynix down 26% from its highs, Western Digital down 32%, Seagate down 29%, Micron down 25%, SanDisk down 30%, Samsung down 21%.

The question every investor in the sector is asking is the one José Luis Cava addresses directly: is this the bottom?

His answer, grounded in a concept borrowed from football analysis, is no. Not yet.

The Dynamics of the Unexpected

Dante Panzeri was an Argentine football journalist whose 1967 book Fútbol: dinámica de lo impensado argued that the most important events in a football match are the ones that contradict what everyone expects to happen. The team that appears dominant, that controls possession, that the crowd expects to win — often loses, precisely because the opponent finds the unexpected path.

Cava applies this concept to markets through a specific technical mechanism. In any sustained correction, price does not simply fall to a fair level and stop. It seeks the points of maximum psychological pain — the levels where the maximum number of participants are holding losing positions, where the pressure to sell has not yet fully expressed itself, where stop-loss orders and forced liquidations are concentrated.

The KOSPI established two reference lows during the current correction: the first at 7,050 on May 20, and the second at 7,400 on June 11. Between those lows, the index attracted buyers — investors who saw value, who noted the support levels, who entered positions expecting recovery. They are now underwater.

The dynamic of the unexpected, applied technically: the market's next move is to go below those levels — to visit 7,050 or below — not because anything has changed fundamentally, but because that is where the stops are. That is where the investors who bought the "obvious" support levels will be forced out. The exhaustion has to be complete, the psychological demoralization has to reach the point where the last willing buyer has either sold or stopped looking, before a genuine base can form.

This is not a prediction that the KOSPI will collapse. It is a description of the mechanical process that markets use to clean out the excess of optimistic positioning before the next meaningful advance. The semiconductor correction that began with the SpaceX IPO rotation has not completed this process. The sweep is still in progress.

What the Memory Sector Data Says

Fernando Sánchez's data makes the correction visible across the entire memory supply chain simultaneously:

SK Hynix: from 1,710 to approximately 1,285 (-26%). Western Digital: -32%. Seagate: -29%. Micron: -25%. SanDisk: -30%. Samsung: -21%.

Several things are notable about this pattern. The breadth is uniform — every significant memory company has fallen by similar magnitudes in the same two-week window. This is not a company-specific problem. It is a sector rotation: capital that had accumulated in memory stocks following the AI infrastructure investment supercycle is exiting systematically, moving into sectors with stronger current momentum — healthcare, insurance, financials.

The second notable aspect is the magnitude. A -25% to -32% correction from recent highs in two weeks is not a minor adjustment. It represents a significant reversal of the gains that memory stocks accumulated when the AI narrative was at its most optimistic. The market is reassessing how much of the HBM memory demand is structural versus how much was a one-time build-out that is now largely fulfilled.

Fernando has been clear throughout the year about this distinction. Memory companies — SK Hynix, Micron, Samsung — are cyclical businesses. Their earnings do not grow steadily year after year. They peak when supply is tight and demand is strong, then compress sharply when customers have built sufficient inventory. The PER of 6-8 that appeared cheap at the peak was a peak-cycle PER, not a normalized one. The correction is the market discovering this, as it always does, after the peak has already been made.

This does not mean these companies are bad businesses. It means the timing of entry matters enormously, and the timing of adding to existing positions matters even more. Averaging into a cyclical correction before the cycle has turned is buying more of what is going down, which is the inverse of sound position management.

Why Waiting for the Signal Beats Acting on the Price

The natural temptation when a stock you own falls 26% is to buy more — to "average down" and reduce your average cost. The math of averaging is compelling in isolation: if you bought at 1,710 and add at 1,285, your average entry is materially lower, and the recovery to 1,710 from the lower average requires a smaller percentage gain to return to breakeven.

The problem is that averaging into a cyclical correction assumes the correction is nearly over. If the KOSPI needs to complete its sweep of the 7,050 level — which is the technical pattern Cava identifies as incomplete — then SK Hynix at 1,285 is not near the bottom. It is partway through the correction. Adding at 1,285 might mean holding a larger position through a further decline to 1,100 or below before the cycle turns.

The combination of Fernando's fundamental caution (memory is cyclical, not structural) and Cava's technical assessment (the KOSPI sweep is unfinished) creates a clear operational conclusion: wait. Not for a specific price level to be reached — price levels alone are insufficient because price can always go lower than expected — but for the technical signal that the sweep has completed. The reversal from the exhaustion low, confirmed by volume and momentum, is the entry signal. The price target approaching is not.

The S&P 500 at 8,000: The Math Behind the Number

While the memory sector correction plays out, the broader market continues to build the case that José Luis Cava expresses with a specific price target: S&P 500 at 8,000.

The target is not generated from a complex model. It comes from a straightforward comparison between nominal economic growth and the risk-free rate — the same framework that Cava applies to justify his "not a bubble" thesis.

The Federal Reserve Bank of New York estimates US real GDP growth at approximately 2.7%. Current inflation runs at approximately 3.5%. The sum — 6.2% nominal growth — is the rate at which the economy is expanding in current dollar terms. Corporate revenues, which are priced in current dollars, grow roughly in line with nominal GDP over a full cycle.

The 10-year Treasury yield is 4.5%. The gap between nominal GDP growth (6.2%) and the risk-free rate (4.5%) is 170 basis points. This is the monetary stimulus embedded in the current environment — the amount by which the productive economy is outpacing the cost of borrowing. When nominal growth significantly exceeds the risk-free rate, capital flows into the assets that benefit from growth: equities.

The S&P 500 at 8,000 represents approximately 10-12% upside from current levels, consistent with a year in which Q2 2026 earnings are expected to exceed already-elevated expectations. The PER of 19 that applies to current prices would, at 8,000, be applied to a higher earnings base — the multiple would not expand much from current levels, but the earnings would. This is earnings-driven appreciation, not multiple expansion, which is the more durable type.

The Michael Dell example that Cava cites is illustrative in its simplicity. A fund that invests $1,000 at birth for every American child, placed into the largest US companies, will outperform the Social Security system's returns on government bonds with high probability over a 65-year horizon. This is not a sophisticated investment thesis. It is the straightforward consequence of equities compounding at nominal GDP growth plus a small premium, versus government bonds yielding below nominal growth.

The 10% historical annual return of the S&P 500 that Cava references is not mysterious — it is approximately equal to the long-run nominal growth rate of the US economy, plus dividends. As long as that economy continues to grow nominally, the index will tend to track it.

Analysis based on José Luis Cava's market commentary and Fernando Sánchez's channel content from July 7, 2026. This post is for informational and educational purposes only and does not constitute investment advice.

Explore the data

Check the latest congressional trades and active investment signals.