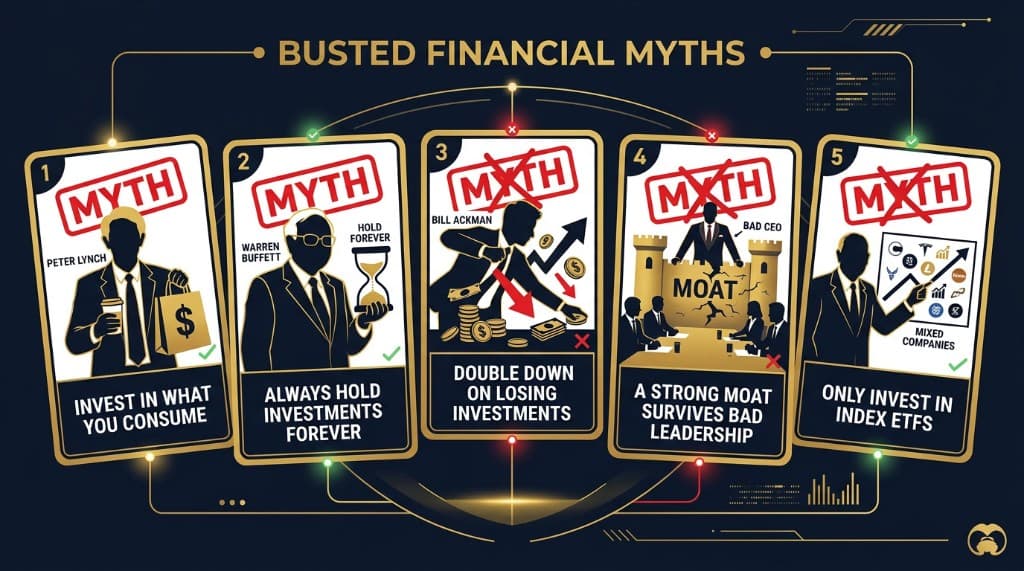

Five Investment Mantras That Can Destroy Your Portfolio If You Follow Them Blindly

Invest in what you consume. Hold forever. Stay convicted. Management doesn't matter. Buy the whole index. Five pieces of advice attributed to legendary investors — Peter Lynch, Warren Buffett, Bill Ackman, Pat Dorsey, Jack Bogle — that are partially true, widely misunderstood, and potentially dangerous when applied without nuance. Fernando Sánchez of Invertir desde Cero dismantles each one.

1. "Invest in what you consume" — Peter Lynch

Peter Lynch popularized the idea that ordinary investors have an edge over Wall Street professionals because they encounter great businesses in their daily lives before analysts discover them. If you love Starbucks coffee or Nike shoes, you might spot the investment opportunity before the institutions do.

The principle sounds compelling. The application is dangerous.

Personal taste tells you almost nothing about investment viability. A business you enjoy as a consumer and a business worth owning as a shareholder are evaluated on completely different criteria: revenue growth rates, margin structure, debt levels, competitive moats, and — most critically — the price you pay relative to the value you receive. None of these factors appear in the experience of drinking coffee or wearing running shoes.

The bias cuts in two directions. It leads investors to ignore genuinely excellent businesses they do not personally use (Meta built one of the most profitable advertising platforms in history; YouTube generates nearly $10 billion per quarter; neither required personal enthusiasm to be a compelling investment). And it leads investors into mediocre or deteriorating businesses simply because they are familiar brands.

The actual Lynch lesson, properly understood, is different: your professional expertise and deep sector knowledge — not your consumer preferences — give you a genuine informational advantage. An engineer who understands the software industry, a nurse who follows pharmaceutical development, a logistics professional who understands supply chain dynamics: these are sources of edge. Personal consumption is not.

2. "My favorite holding period is forever" — Warren Buffett

This is the most misquoted investment principle in the history of finance. The misreading converts a nuanced statement about quality into a passive instruction to never sell anything.

Buffett's actual approach is nothing like buy-and-forget. Berkshire Hathaway monitors its positions constantly, has sold significant stakes in major holdings when valuations became stretched or when the investment thesis changed, and applies rigorous ongoing analysis to every position.

Fernando's framing is more honest about what the discipline actually requires: buy and watch, not buy and forget. This means reviewing fundamentals and intrinsic value estimates quarterly — earnings growth, margin trends, competitive position, management decisions — and being willing to act on what you find.

The key insight on selling: if a company reaches in one year the price target you had set for five years — driven by market euphoria rather than fundamental improvement — the rational action is to sell and redeploy capital toward opportunities with greater margin of safety. The stock is a vehicle for capital growth, not a relationship requiring loyalty. When the vehicle has delivered its expected journey ahead of schedule, you move to the next one.

3. Conviction versus ego — the Bill Ackman warning

The line between disciplined conviction and destructive stubbornness is one of the most important distinctions in investment psychology, and one of the hardest to draw in real time.

Ackman provides the clearest case study. His position in Valeant Pharmaceuticals — held and compounded as regulatory scrutiny intensified, accounting questions multiplied, and the business model deteriorated visibly — resulted in losses exceeding one billion dollars. The information that should have triggered exit was available. The ego investment in being right prevented acting on it.

The same pattern appeared in his short position on Herbalife, a high-conviction bet held through accumulating evidence that the thesis was not playing out as expected.

The distinction that matters: maintain conviction when the reasons for a price decline do not change the original investment thesis. Exit when the thesis itself has been invalidated by new information — when the facts that justified the position no longer hold. The test is not "is the stock down?" It is "is the reason I bought it still true?"

Ackman's error was not having conviction. It was holding conviction through thesis invalidation rather than through ordinary price volatility.

4. Management is a critical competitive advantage — against Pat Dorsey

The conventional view in fundamental analysis, associated with Pat Dorsey, holds that competitive moats — brand, network effects, switching costs, cost advantages — are structural and persist largely independent of who runs the business. Good management accelerates; bad management decelerates. But the moat does the work.

Fernando's counter-argument, supported by specific cases, is that management can both build and destroy moats at a pace that this framework underestimates.

Nike is the evidence. Under CEO John Donahoe, a series of strategic decisions — shifting away from wholesale distribution toward direct-to-consumer too aggressively, deprioritizing sports performance marketing, cutting relationships with specialty retailers — eroded the brand's market position in ways that took years to develop and cannot be quickly reversed. The stock fell approximately 70% from its peak. The brand itself had not deteriorated. The decisions made about how to manage it had.

Cegona/Vodafone Spain is the counter-example. A structurally mediocre telecommunications business — commoditized product, intense competition, limited differentiation — was acquired and managed by a team that executed aggressive cost restructuring and operational improvement. The stock returned approximately 200%. The business had not changed. The people running it had.

The moat does not defend itself. It requires capable people making correct decisions. Ignoring management quality in favor of structural analysis alone leaves a significant variable unexamined.

5. "Don't look for the needle, buy the haystack" — Jack Bogle

Bogle's argument for index investing — that most active managers fail to beat the market over time, making the diversified index the rational choice for most investors — is empirically well-supported and genuinely useful advice for the majority of people who have no interest in stock analysis.

Two complications are worth noting.

The conflict of interest: Bogle created and sold the products he recommended. This does not make the advice wrong, but it is a relevant fact when evaluating the source.

The composition problem: The S&P 500 index contains Apple, Microsoft, Nvidia, Visa, and Amazon — some of the most profitable and well-managed businesses in history. It also contains hundreds of companies that are mediocre, heavily indebted, structurally declining, or operating in industries being disrupted. Buying the index means owning both categories in fixed proportion, with no ability to concentrate in what works and avoid what does not.

For an investor willing and able to do rigorous fundamental analysis, selective portfolio construction — concentrated in high-quality businesses purchased at reasonable valuations — offers a demonstrable theoretical advantage over owning the entire market. The difficulty is executing the analysis correctly and consistently. Most investors cannot. For those who cannot, the index is the right answer. For those who can, it is an unnecessary constraint.

Analysis based on content published by Fernando Sánchez of Invertir desde Cero, June 2026. For informational purposes only — not financial advice.

Explore the data

Check the latest congressional trades and active investment signals.