Investors Trust NVIDIA More Than the US Government — And How to Know When the Market Is Really in Danger

The Financial Times reported something extraordinary: the risk premium on NVIDIA's 5-year debt is lower than that of US government bonds. Private enterprise is now considered safer than the sovereign. José Luis Cava explains why this makes sense, why AI is still not a bubble, and introduces the one tool that separates real market danger from manufactured fear: Credit Default Swap premiums on high-yield debt.

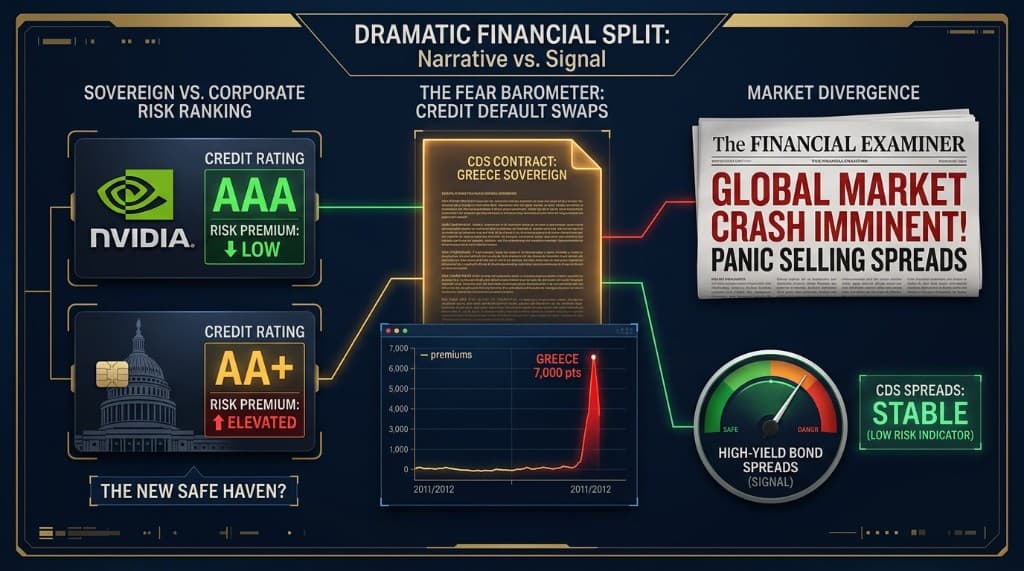

The data point that reframes everything

The Financial Times published a figure that deserves to stop you mid-scroll: the risk premium demanded by bond investors for NVIDIA's 5-year debt is lower than the equivalent for US government bonds.

Let that settle. The United States government — which can levy taxes on the entire economic output of the world's largest economy and, in extremis, print its own currency — is considered by credit markets to be a worse credit risk than a single technology company headquartered in Santa Clara.

Cava's reading: this is not an anomaly or a pricing error. It is the rational conclusion of two simultaneous realities. The first: NVIDIA has demonstrated consistent solvency and earnings growth over the past decade, and the AI revenue pipeline ahead of it is among the most visible in corporate history. The second: the US government is running a 6% of GDP deficit with no credible path to primary surplus, and its interest burden is projected to grow from 3.2% to 3.6% of GDP over the next decade.

One of these entities is generating cash and growing. The other is compounding debt. Credit markets are simply reflecting the mathematics.

The contrarian signal: mockery means the trend continues

Cava invokes the contrarian opinion theory to address the persistent bubble narrative around AI.

The theory is simple and historically durable: when a trend is genuinely approaching exhaustion, the people who have been riding it become complacent and the skeptics go quiet — because the skeptics have either capitulated or been discredited. When a trend is still intact and has significant upside remaining, the public discourse is dominated by mockery, skepticism, and comparisons to historical bubbles.

The current AI debate is overwhelmingly characterized by bubble comparisons and dismissal. Financial media publishes dot-com overlays. Commentators cite Nvidia's valuation multiples without accounting for its earnings growth. The retail investor public largely believes the rally is manufactured.

In Cava's framework, this is the signal that the trend is not finished. Charts of the semiconductor sector, cybersecurity, memory, and optics show no technical exhaustion — no distribution patterns, no divergences, no breadth deterioration of the kind that precedes genuine reversals. The narrative says bubble. The price action does not.

Credit Default Swaps: the dark side of speculation

Cava introduces CDS instruments as a tool that most retail investors have heard of only in the context of the 2008 crisis, without understanding their actual mechanics.

A Credit Default Swap is, in its original form, an insurance contract on a bond. If you hold a bond from a corporation or government, you can purchase a CDS to protect against default — if the issuer fails to pay, the CDS seller compensates you.

The "dark side" that Cava identifies is structural: you can buy a CDS without owning the underlying bond. This transforms an insurance instrument into a pure speculation vehicle. You are not hedging an exposure you have — you are betting that someone else will fail to pay their debt.

The mechanics of the CDS market connect directly to the liquidity cycle. When liquidity is abundant — when central banks are injecting money and risk appetite is high — default probabilities fall, and CDS premiums fall with them. When liquidity contracts, default risk rises, and CDS premiums spike.

The Greece case study: From 2008 onward, Greek sovereign CDS premiums were low. But the chart of those premiums was in a clear upward trend — the price was rising even when the absolute level was still modest. Cava recognized this as the signal: the market was slowly pricing in the deterioration of Greek public finances that the official narrative was denying. He built a position. The CDS eventually reached 7,000 points. He sold when the story went mainstream — when Varoufakis was appearing on every television channel and the Greek crisis was front-page news globally. By the time the public understood what was happening, the trade was over.

The AIG case study: AIG sold CDS contracts on US mortgage bonds at scale, convinced that a nationwide housing crash was impossible. The logic was the same as every bubble: the underlying asset cannot fall because it has never fallen before. When the mortgage market collapsed in 2008, AIG had sold more insurance than it could pay. The US government intervened to prevent the systemic collapse that AIG's failure would have caused. The lesson: being the seller of unlimited CDS on a bubble asset is existential risk.

The practical tool: watch high-yield CDS premiums

For investors who are not operating in credit markets directly, the CDS framework provides a practical monitoring tool that is more reliable than any media narrative.

When someone warns of imminent market collapse, check the CDS premiums on high-yield (junk) bonds.

High-yield CDS premiums reflect the market's collective assessment of default probability across the riskiest segment of corporate debt. When systemic risk is genuinely rising — when the financial system is actually moving toward stress — these premiums begin trending upward. They do not lie, because the people pricing them have real money at stake.

The test Cava applies: if media coverage is generating fear about a market collapse but high-yield CDS premiums are not in a clear upward trend, the fear is narrative, not signal. The market is being manipulated by words, not by the underlying credit mechanics.

Applied to recent history: during the correction episodes of April 2025 and March 2026, the fear narrative was intense. But CDS premiums on high-yield debt did not confirm a systemic deterioration. The corrections were sweeps — mechanical clearing of weak hands — not the beginning of a credit cycle reversal.

The real signal, when it comes, will appear in the CDS premiums before it appears in the headlines. That is the edge.

Analysis based on a José Luis Cava video published June 2, 2026. For informational purposes only — not financial advice.

Explore the data

Check the latest congressional trades and active investment signals.