Oil: The Market Priced a Peace That Doesn't Exist Yet — And Cushing Is About to Run Dry

José Luis Cava identifies a dangerous mispricing in oil markets: traders have liquidated long positions and priced in the best possible scenario from the US-Iran agreement, but what will be signed in Geneva is a non-binding Memorandum of Understanding, not a peace treaty. Meanwhile, US strategic reserves sit at 1983 lows, and the Cushing, Oklahoma delivery hub is on track to breach 20 million barrels — the operational damage threshold — by June 19-20. The shorts are standing on sand. Add Japan's paradox (rates up, liquidity still flowing) and France's structural euro problem, and the macro picture is more volatile than markets suggest.

A memorandum is not a peace treaty

The oil market has moved in two stages. First, speculative long positions — bets on rising oil prices — accumulated massively as Middle East tensions escalated. Then, as the US-Iran framework began to emerge, those same positions were liquidated en masse, with the market pricing in the most optimistic possible reading: full resolution of the conflict and an immediate return to normalized energy flows.

The problem, according to Cava, is that what will actually be signed in Geneva is a Memorandum of Understanding — a MoU. A MoU is not a binding agreement and not a treaty. It establishes lines of cooperation and creates the framework for negotiation, but it carries no legal enforcement mechanism. Following its signature, both parties will have a further 60 days to negotiate the real agreements, a process that can be extended indefinitely through the ordinary mechanics of political negotiation.

During those 60 days, each side will use oil as leverage. Iran will push for sanctions relief. The United States will push for specific nuclear and missile commitments. Saudi Arabia and the Gulf states will watch their market share calculations. Every headline from every negotiating session will move the Brent price. The market has priced in the destination before the journey has even begun.

The consequence is a technically fragile setup: long positions have collapsed to pre-conflict levels, futures structures project prices of $70-75 for the coming months, and bears control the narrative. But the fundamental picture does not support this positioning.

Trump has run out of physical ammunition

The United States has historically used the Strategic Petroleum Reserve (SPR) as a tool for suppressing oil prices during political pressure periods — releasing barrels into the market to increase supply and dampen price spikes. This tool is no longer available.

Current SPR inventories have reached their lowest levels since August 1983. The reserve that was once large enough to influence global supply dynamics for months has been drawn down through successive releases. Trump can still apply pressure in the paper markets — through signals, diplomacy, and forward guidance — but he cannot physically suppress prices through SPR releases without creating a national security risk.

This matters because the bullish case for oil does not require extraordinary events. It only requires the absence of artificial suppression. With the SPR exhausted, the market is left to price oil based on actual supply and demand.

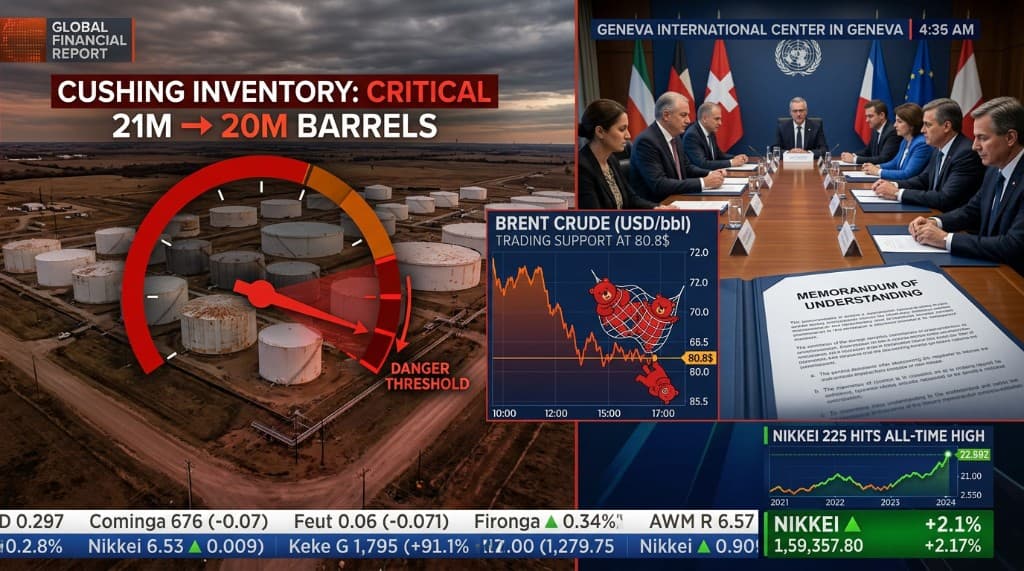

Cushing is approaching the operational damage threshold

The most immediate and concrete risk in this analysis sits at Cushing, Oklahoma — the physical delivery hub for NYMEX crude oil contracts and the central logistical node of the American oil market.

Inventories at Cushing follow a precise trajectory: 21.6 million barrels on June 5, dropping to 21 million on June 12. Cava's team estimates that inventories will fall below 20 million barrels between June 19 and June 20. The 20 million barrel level is not arbitrary — it represents the operational threshold below which pipeline and storage infrastructure can sustain physical damage. Tank bottoms, pump minimums, and pressure maintenance requirements all become critical below this level.

The structural implication for traders is significant: anyone currently holding short positions on crude expects to deliver — or roll — contracts against a physical market that is approaching a genuine scarcity event at the primary delivery point. When Brent spot has held above the March lows of $79.7 and trades at $80.8 despite the avalanche of bearish sentiment, the market is already sending a warning that the physical reality does not match the paper positioning.

Cava's forecast: the next 63 days — the 60-day MoU negotiation window plus the lead-up days — will generate a period of high probability for significant upward oil price moves, as both negotiating parties apply pressure and physical constraints tighten.

The Japan paradox: rates up, liquidity still flowing

One of the clearest signals about global liquidity is visible in Japan. The Bank of Japan has raised interest rates — a decision that generated significant concern about the reversal of the yen carry trade and a potential liquidity drain from global risk assets. The prediction was that higher Japanese rates would trigger yen appreciation, forcing the unwinding of leveraged positions funded in yen, with destabilizing consequences for equity markets worldwide.

The Nikkei's behavior has flatly contradicted this narrative. The Japanese equity index continues to mark all-time highs. The reason is that the BoJ, while raising policy rates, has simultaneously continued to inject liquidity through its balance sheet — purchasing assets and maintaining the monetary base that supports financial conditions. The headline rate increase is real. The net monetary effect is not tightening. The Bank of Japan is raising rates with one hand while maintaining accommodation with the other.

For global markets, this matters: the world's third-largest economy and one of the primary sources of global carry funding is not withdrawing liquidity. The risk of a yen-driven deleveraging event that would drain liquidity from emerging markets and risk assets is substantially lower than the rate headlines suggest.

France and the structural euro problem

Cava closes with a structural observation about European fiscal credibility. France currently maintains a fiscal deficit exceeding 6% of GDP despite operating one of the heaviest tax burdens in the developed world. The political economy of France demonstrates concretely that high taxation does not automatically produce fiscal balance when structural spending commitments remain unaddressed.

The consequence for the euro is a slow-moving structural pressure. When a major eurozone economy maintains deficits of this scale persistently, it creates sovereign risk, adds pressure to European bond markets, and ultimately undermines confidence in the currency union's fiscal coherence. The ECB's recent rate hike — already identified as a policy error — becomes more problematic in this context: tightening monetary conditions while fiscal policy remains structurally loose is not a credible combination.

For investors with euro-denominated assets, this is an argument for maintaining exposure to global earnings rather than European domestic revenue streams.

The operative picture for June 16

Oil shorts are structurally exposed: they have priced a peace that is legally a preliminary framework, positioned against a physical market approaching an operational stress threshold, with the US government's primary suppression tool exhausted. The summer will not be quiet in energy markets.

Japan's paradox reinforces that global liquidity conditions remain more accommodative than surface readings suggest. France's deficit reinforces euro structural weakness. Both arguments support the broader thesis: US dollar strength, global growth continuation, and the 18-24 month bullish window for quality growth equities remains intact despite near-term tactical noise.

Analysis based on José Luis Cava video published June 16, 2026. For informational purposes only — not financial advice.

Explore the data

Check the latest congressional trades and active investment signals.