SpaceX Is Three Companies in One — and the Math Does Not Work at $2 Trillion

SpaceX's IPO is arriving in one of the most euphoric markets in history — Micron up 197% in 2026, SanDisk up 4,200% in twelve months. Fernando Sánchez cuts through the narrative with the actual financial data: SpaceX is three businesses with radically different economics, consolidated losses of $4.9 billion, and a valuation of 43 to 46 times sales. The three golden rules for anyone who still wants exposure, and why the lockup expiration — not the listing date — is where the real opportunity begins.

2026: the year the exit doors opened

Three of the most anticipated private technology companies in history are preparing to go public in 2026: SpaceX, OpenAI, and Anthropic. The financial media is presenting this as a historic investment opportunity. Fernando Sánchez's analysis inverts that framing entirely.

The IPO is not primarily a mechanism for companies to raise capital for growth. It is primarily a mechanism for founders, employees, and venture capital funds to convert years of illiquid private stakes into cash. The people who know the business best — who built it, who understand its risks most intimately — are selling. The people who know it least are buying.

This is not cynicism. It is the structural reality of how equity markets function at the IPO stage.

The banks that are not working for you

The investment banks managing the SpaceX offering — Goldman Sachs, Morgan Stanley, JP Morgan — earn between 5% and 7% of the total capital raised. On a $75 billion offering, that is between $3.75 billion and $5.25 billion in fees. Their client is SpaceX and its existing shareholders, not the retail investor purchasing shares at the offering price.

Their incentive is explicit: the higher the IPO price, the more capital is raised, the higher their fee. Every dollar of optimism baked into the offering price benefits the banks. None of the downside falls on them.

Understanding whose interests are aligned with whose is the first step in evaluating any IPO.

The market that makes this possible

The IPO wave is landing in exceptionally fertile conditions. 2026 has produced some of the most extreme individual stock returns in recent memory:

- Micron: +197% in 2026, +870% over twelve months

- SanDisk (Western Digital spin-off): +4,200% in twelve months

These are not business results. These are speculative moves in a market saturated with AI narrative and capital that needs somewhere to go. This environment — what Fernando calls a "drunk market" — is the optimal moment to launch an IPO. The appetite of investors is at its maximum. The ability to price assets rationally is at its minimum.

The statistical reality of IPO investing

The Renaissance IPO ETF, which tracks the performance of newly listed companies, provides the most useful aggregate data available:

- Since 2013: 8% annual return versus 12.4% for the S&P 500

- Last five years: -2.6% annual return versus +12.3% for the market

This is not a selection of failed companies. This is the full universe of IPOs. The average IPO, held as part of a diversified basket, has underperformed the market by more than four percentage points annually since 2013 — and has produced negative absolute returns over the past five years.

Jay Ritter's academic research, the most comprehensive longitudinal study of IPO performance, finds that after three years, IPOs generate returns 20.5% below the market average. For companies that go public without profitability — which describes many of the highest-profile recent listings — the underperformance reaches 30.7%.

The survivors that investors remember — Amazon, Tesla, Nvidia — exist against a backdrop of thousands of companies that failed or permanently underperformed. Survivorship bias makes IPO investing appear more rational than the data supports.

SpaceX: three companies with three very different realities

The most important analytical contribution of Fernando's analysis is the decomposition of SpaceX into its constituent businesses. The consolidated entity obscures three fundamentally different financial profiles:

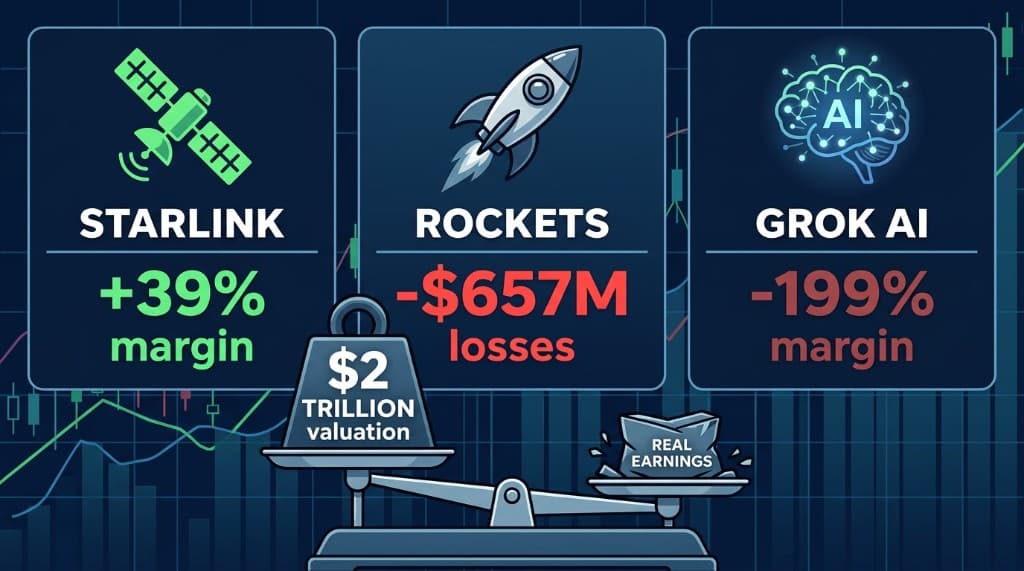

Starlink (the jewel): $11.4 billion in revenue in 2025, with a 39% operating margin. This is a genuine, profitable, rapidly growing business — a global satellite internet provider with pricing power and no viable competitor at scale. If Starlink were an independent public company, it would be one of the most attractive technology listings in years.

Aerospace (rockets and launch): Despite being the global leader in launch vehicle reuse, this division generates operating losses of $657 million annually. The development costs of Starship — the next-generation system designed to make Mars missions economically viable — consume the cash that the rocket business generates.

Grok (AI): Revenue of $3.2 billion, but operating losses of $6.3 billion, producing an operating margin of -199%. The AI division is consuming nearly twice its revenue in expenses. At scale, this may generate transformational returns. At the IPO valuation, investors are being asked to fund losses of $6.3 billion per year in a division with no clear path to profitability.

Consolidated: The company grows at 33% annually — impressive by any standard. But it carries consolidated operating losses of $4.9 billion. The proposed valuation of $1.7 to $2 trillion implies a multiple of 43 to 46 times revenue — not earnings, revenue. To justify this multiple, SpaceX's management cites a total addressable market of $28.5 trillion, a figure that would represent approximately 90% of US GDP. The mathematics are not credible.

The three golden rules

Fernando's framework for the rare investor who still wants SpaceX exposure through any vehicle that emerges:

Rule one: never buy on day one. The first day of trading is the moment of maximum euphoria and minimum information. The price reflects marketing, not analysis. It is the worst possible moment to make a capital allocation decision.

Rule two: wait for the lockup expiration. Regardless of the specific structure — standard 180-day lockup, staged lockup, or immediate selling rights — the moment when insiders begin systematically exiting is the moment that reveals the real supply-demand balance. Historically, the peak-to-trough decline from IPO high to post-lockup low reaches approximately 55%. That correction is the beginning of a rational price discovery process, not the end of an investment opportunity.

Rule three: wait for two to three quarters of audited results. Public companies must report real numbers, reviewed by independent auditors, quarterly. After two or three reporting cycles, the gap between IPO narrative and business reality becomes visible. The companies that deserve capital allocation reveal themselves through their numbers. So do the ones that do not.

What the data means for positioning

The June 12 listing date is not an investment signal. The lockup expiration — and the potential Q2 results publication in late July or August, in thin summer markets — is where the correction begins that creates rational entry points.

For European investors seeking structured exposure to the space sector without the IPO risk, the analysis points toward vehicles like JEDI (VanEck), which will absorb SpaceX into its portfolio through index inclusion after the listing, at prices that reflect post-IPO reality rather than day-one euphoria.

The three golden rules are not pessimism about SpaceX as a business. Starlink alone may justify a significant long-term valuation. They are a discipline about price — the principle that the quality of a business and the quality of an investment are different questions, and that the IPO date is almost never the answer to the second one.

Analysis based on a Fernando Sánchez video published June 7, 2026. For informational purposes only — not financial advice.

Explore the data

Check the latest congressional trades and active investment signals.